Rarely a day goes by where an incidence of supply chain disruption isn’t discussed in the media, particularly the semiconductor industry’s woes owing to the COVID-19 pandemic. Supply chain research has often centered on shock transmission, how events like the earthquake in Japan or Thai floods in 2011 affect firms’ supply chains. However, missing from the equation are insights into how firms are affected by supply chain risk—quantified at the firm level—and how they respond. New co-authored research by SMU Cox Assistant Professor of Finance Ruidi Huang reveals novel insights into the nature of supply chain risk. “No one really knows the real supply chain risk at the firm level,” Huang emphatically states.

During the pandemic, still ongoing since 2019, the amount of discussion of supply chain is very elevated among firms, and in the media. The authors write:

… Though both the academic literature and recent events highlight that supply chain shocks are an important source of disruption, we know little about whether firms systematically update their investors about [this source of risk]… Concerns have been raised that due to the complexity of supply chains, firms are often unaware of the supply chain risks their suppliers are subject to and may consequently not be able to manage this source of risk.

A cool proxy

Huang and his co-authors develop a proxy to measure supply chain risk. “The way in which we assess supply chain risk is unique in the academic literature,” Huang says. They analyze instances of supply chain mentions in earnings calls of publicly-traded firms’ transcripts, which speaks to “sentiment.” Secondly, they analyze risk and uncertainty associated with those supply chain mentions. Machine learning techniques and word clouds are utilized to guide their quantification of supply chain risk for the firm. While disruptive effects manifest system-wide and in day-to-day purchasing situations, the firm level measure reveals a lot of where the action is.

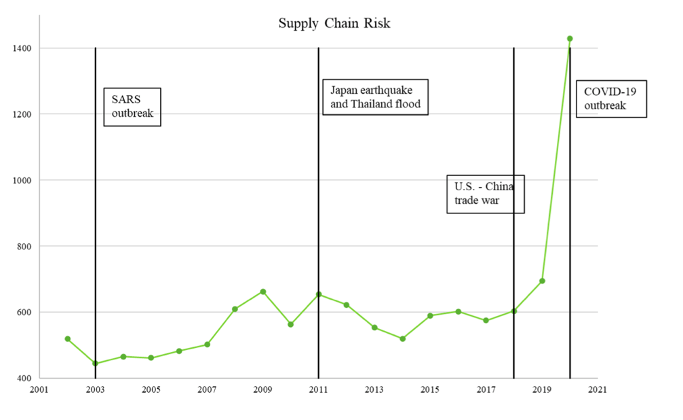

Supply chain risk appears to be heightened and sentiment becomes more negative in connection to events that are disruptive to global supply chains, such as the 2011 great East Japan earthquake and the Thailand floods, the Sino-American trade war, and more recently with the Covid-19 outbreak. Surprisingly, the 2003 SARS outbreak did not move the needle much. But that was also a time of less social media intensity.

“Supply chain risk is not one-sided,” the authors note. There are firms and periods with positive supply chain sentiment, with opportunities for outsourcing to reduce costs, and also of negative sentiment when concerns about bottlenecks and the reliability of the supply chain emerge. The pandemic laid bare the reliability of supply chains globally. Additionally, supply chain risk does not simply arise from transportation costs.

Firms respond to risk

According to the research, manufacturing industries are the most sensitive to supply chain risk. Think textiles, machinery, hi-tech, minerals. In particular, the pandemic revealed a “flight to quality.” When faced with supply chain risk, the research finds that firms seek out leaders in their industry. The trend toward reshoring is a byproduct of supply chain risk. The larger story however is the drive toward supply chain resiliency.

Huang and co-authors document how firms respond to supply chain risk. Their work helps explain why Tesla seeks to buy firms that contribute to their smoother operations strategically.

To address supply chain risk, firms increase investment in the supply chain, which includes increased merger and acquisition (M&A) activities such as buying suppliers. They increase their number of suppliers, that is “multi-sourcing,” which also diversifies the chain. Heightened supply chain risk leads to the movement toward greater geographic proximity and aligning with industry leaders as well, a key point in the research.

A number of significant firsts can be claimed by the authors. One is quantifying supply chain risk at the firm level by using machine learning techniques to identify instances of supply chain risk. A second unique finding is that supply chain risk is a driver of vertical integration. The study considers M&As with firms in up and downstream industries. They find that an increase in supply chain risk leads to a higher probability of M&As; this probability of an M&A with a supplier or a customer increases by around 25% relative to the baseline merger probability of less than 1%, generally speaking.

Additionally, supply chain risk and sentiment are driven by idiosyncratic risk—at the firm level. While Huang notes that macroeconomic shocks matter, the way firms discuss supply chain risk appears to be highly idiosyncratic. “Most of the variation in supply chain risk is explained by firm-specific shocks rather than time- or industry-specific shocks,” the researchers say in their paper. The authors conclude that shocks to the supply chain at the firm level correspond to proxies similar to that found in the case of political and climate risk. The long-standing practice across the decades of just-in-time operations is debunked as well.

In the future, the authors intend to develop a publicly-available database that will identify the supply chain risk of individual firms throughout the world. This metric will be a timely measure given the increased awareness of how systemic and even globally-regional shocks affect our economic lives.

The paper, “Supply Chain Risk: Changes in Supplier Composition and Vertical Integration,” is authored by Ruidi Huang of Southern Methodist University’s Cox School of Business, Nuri Ersahin of Michigan State University, and Mariassunta Giannetti of Stockholm School of Economics.

Written by Jennifer Warren.

Magazine

Recommended

Subscribe for updates